Page 49 - Monaco Economie 125

P. 49

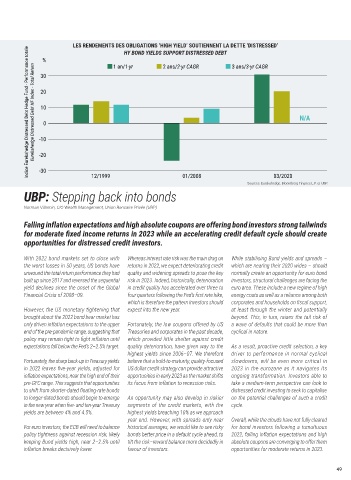

LES RE EME TS ES BLI ATI S I IEL ’ S TIE E T LA ETTE ISTRESSE ’

HY BOND YIELDS SUPPORT DISTRESSED DEBT

% 1 an/1-yr 2 ans/2-yr CAGR 3 ans/3-yr CAGR

Eurekahedge Distressed Debt HF Index - Total Return Indice Eurekahedge Distressed Debt Hedge Fund - Performance totale -10 N/A

30

20

10

0

-20

-30

12/1999 01/2008 03/2020

Sources: Eurekahedge, Bloomberg Finance L.P. et UBP.

UBP: Stepping back into bonds

Norman Villamin, CIO Wealth Management, Union Bancaire Privée (UBP)

Falling inflation expectations and high absolute coupons are offering bond investors strong tailwinds

for moderate fixed income returns in 2023 while an accelerating credit default cycle should create

opportunities for distressed credit investors.

With 2022 bond markets set to close with Whereas interest rate risk was the main drag on While stabilising Bund yields and spreads

the worst losses in 50 years, US bonds have returns in 2022, we expect deteriorating credit which are nearing their 2020 wides should

unwound the total return performance they had quality and widening spreads to pose the key normally create an opportunity for euro bond

built up since 2017 and reversed the sequential risk in 2023. Indeed, historically, deterioration investors, structural challenges are facing the

yield declines since the onset of the Global in credit quality has accelerated over three to euro area. These include a new regime of high

Financial Crisis of 2008 09. four quarters following the Fed’s first rate hike, energy costs as well as a reliance among both

which is therefore the pattern investors should corporates and households on fiscal support,

owever, the US monetary tightening that expect into the new year. at least through the winter and potentially

brought about the 2022 bond bear market has beyond. This, in turn, raises the tail risk of

only driven inflation expectations to the upper Fortunately, the low coupons offered by US a wave of defaults that could be more than

end of the pre-pandemic range, suggesting that Treasuries and corporates in the past decade, cyclical in nature.

policy may remain tight to fight inflation until which provided little shelter against credit

expectations fall below the Fed’s 2 2.5% target. quality deterioration, have given way to the As a result, proactive credit selection, a key

highest yields since 2006 07. We therefore driver to performance in normal cyclical

Fortunately, the sharp back-up in Treasury yields believe that a hold-to-maturity, quality-focused slowdowns, will be even more critical in

in 2022 leaves five-year yields, adjusted for US dollar credit strategy can provide attractive 2023 in the eurozone as it navigates its

inflation expectations, near the high end of their opportunities in early 2023 as the market shifts ongoing transformation. Investors able to

pre-GFC range. This suggests that opportunities its focus from inflation to recession risks. take a medium-term perspective can look to

to shift from shorter-dated floating-rate bonds distressed credit investing to seek to capitalise

to longer-dated bonds should begin to emerge An opportunity may also develop in riskier on the potential challenges of such a credit

in the new year when five- and ten-year Treasury segments of the credit markets, with the cycle.

yields are between 4% and 4.5%. highest yields breaching 10% as we approach

year end. owever, with spreads only near Overall, while the clouds have not fully cleared

For euro investors, the ECB will need to balance historical averages, we would like to see risky for bond investors following a tumultuous

policy tightness against recession risk, likely bonds better price in a default cycle ahead, to 2022, falling inflation expectations and high

keeping Bund yields high, near 2 2.5% until tilt the risk reward balance more decidedly in absolute coupons are converging to offer them

inflation breaks decisively lower. favour of investors. opportunities for moderate returns in 2023.

49